Steps For Home Loan Refinancing, everything you need to know!

Steps For Home Loan Refinancing, everything you need to know!

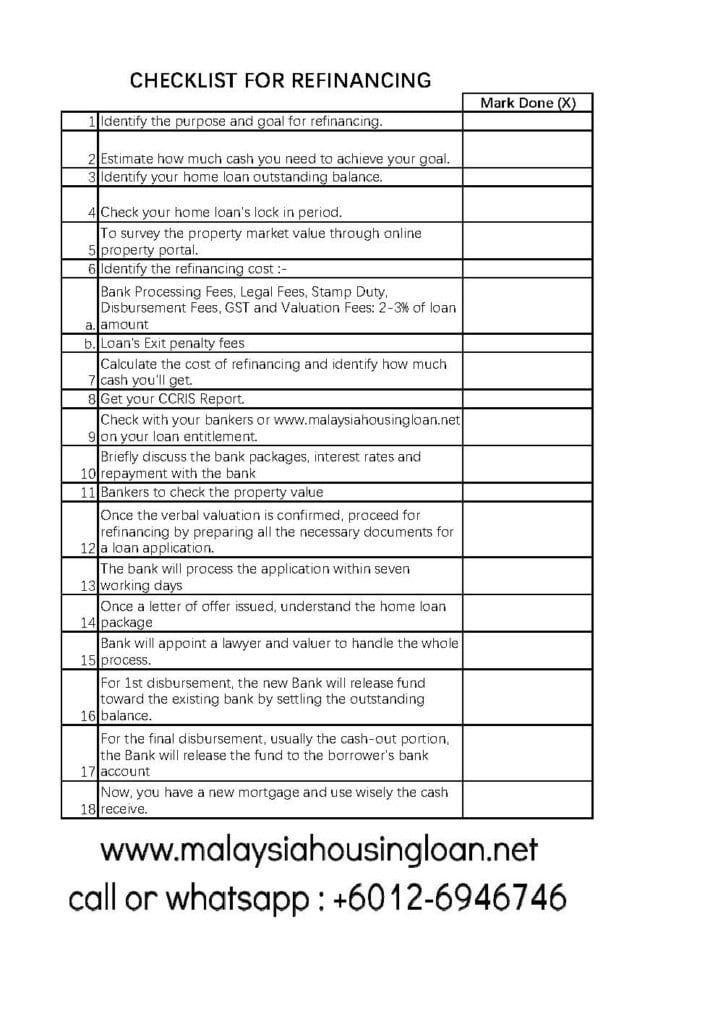

1. Identify the purpose or goal of refinancing. It can be for getting extra cash to pay off the existing high-interest rates loan facility, house renovation, children education, to get lower rates, etc…

If you have a clearer purpose of refinancing, the chances to achieve your target is higher if you make it clear in the early stage.

2. Estimate how much cash you’ll need to achieve your goal. Write it down so that you’ll remember that the cash you get from refinancing is for the purpose that you list out earlier. To avoid of misused the refinancing cash out.

3. Identify your home loan outstanding balance. You can refer to the home loan statement, or you can call up the bank to check.

4. Make sure the lock-in period with the bank is over. If the home loan still under lock-in period, clarify how much you need to pay if proceed for refinancing and check on the lock-in period expiry date.

5. To survey the property market value through online property portal.

You can visit iproperty.com or propertyguru.com to check the selling price in your neighborhood.

From the price you get, try to less 20% from it. That should be the estimate market value for your property. You can use this to make a rough calculation.

Once you apply for a bank loan, you can ask the bankers to double check the property market value to have more accurate value.

Example,

RM600,000 – 20% = RM480,000

6. Refinancing has a cost. Identify the cost, or you can estimate the cost by following the below calculation.

Bank Processing Fees, Legal Fees, Stamp Duty, Disbursement Fees, SST and Valuation Fees: 2-3% of loan amount

Loan’s Exit penalty fees: If any. Check with your bank. Tip: Try to refinance after the lock-in period to avoid exit penalty fees.

7. Calculate the cost of refinancing and identify how much cash you’ll get.

For Example,

Estimate Property Value : RM480,000

Bank’s maximum margin : up to 80%-90% (varied from bank)

Loan Amount to apply : RM480,000 x 90% = RM432,000

Home loan outstanding balance : RM250,000

Bank Processing Fees, Legal Fees, Stamp Duty, Disbursement Fees, SST and Valuation Fees : 3% x 432,000 = RM12,960.00

Loan’s Exit penalty fees : RM5000

Cash out will get: RM164,040.00

Cost of refinancing are,

Bank Processing Fees, Legal Fees, Stamp Duty, Disbursement Fees, SST and Valuation Fees : 3% x 432,000 = RM12,960

Loan’s Exit penalty fees: RM5000

Total: RM17,960.00

8. Get your CCRIS Report. Three ways to get your CCRIS report.

a. Walk into Bank Negara and get your CCRIS report print.

b. Fill up a form and send an email to Bank Negara, request a CCRIS report. You’ll receive within 14 days.

c. You can go to www.ctoscredit.com.my and get your CCRIS report print with a minimum fee.

CCRIS report is critical as the bank will be based on your CCRIS report to provide a financing. It’s so important that it stands 50% chances of approval rating.

9. Check with your bankers or www.malaysiahousingloan.com on your loan entitlement. Let’s us evaluate your CCRIS report and your eligibility to borrow, based on existing income, expenses and other loan repayment commitments.

Having a good credit record by keeping all payments up to date on existing credit facilities/ liabilities is a plus point.

10. Briefly discuss the bank packages, interest rates and repayment with the bank. Tip: Do not compare your interest rates upfront with the bank. Get an approval with the banks and compare. Approval from the bank is more important. No point to compare if the bank will not approve your loan.

11. If everything looks good, ask the bankers to check the property value. Make sure it matches the previous value. If it doesn’t match, do your calculation again and ask for the banker to negotiate with their valuer for higher value.

12.Once the verbal valuation is confirmed, proceed for refinancing by preparing all the necessary documents for a loan application. Such as: Tip: Verbal valuation is not 100% accurate. Once a customer has accepted the bank letter offer, the bank will arrange a valuer to inspect the property. A valuation report with a confirm value will be submitted to the bank.

For Under Employment:

(Meaning working with company or receive a fixed monthly income)

1. NRIC copy

2. Sales and Purchase Agreement / Title copy

3. Latest 3 months pay slips (For Basic Salary) / Latest 6 months pay slips (For Basic + Commission-Earner)

4. Latest 3 months personal bank statement (For Basic Salary) / Latest 6 months pay slips (For Basic + Commission-Earner)-(To show salary credited as per pay slip)

5. Latest EA form / Employment Letter

6. Latest KWSP statement

7. Income Tax-Latest Form B / BE with payment receipt acknowledgment

8. Latest six months Housing Loan Statement. (If the property still charged to bank)

9. Letter Offer from the previous bank. (If the property still charged to bank)

13. The bank will process the application within seven working days ( depend on banks might be varied). A letter of offer will be issued if the application is approved.

14. Once a letter of offer issued, understand the terms and conditions, such as interest rates, package, lock-in period, loan amount, refinancing cost, additional fees, monthly or daily rest, Islamic or conventional loan, etc.

Try to ask as many questions as possible to the bankers. Because it’s important to understand the whole package before signing the offer. Tip: At this stage, you can compare the interest rates among banks.

15. Bank will appoint a lawyer and valuer to handle the whole process. Usually, for freehold property with strata/individual title, it will take about 3-4 months, and leasehold property with strata/individual title is about 5-6 months. Tip: Leasehold property with strata/individual title issued need to apply consent from the state. It will take about 2-3 months time just to get approval from the State. But, on a rare occasion, there were cases up to 6 months to get consent.

16. For 1st disbursement, the new Bank will release fund toward the existing bank by settling the outstanding balance. Afterward, the existing bank will release all the old agreement and forward to the bank lawyer.

17. For the final disbursement, usually the cash-out portion, the Bank will release the fund to the borrower’s bank account.

18. Now, you have a new mortgage and use wisely the cash receive.

Good Luck!

Check out our checklist for refinancing here.

If you think this is helpful, feel free to share it with all your friends and family on all the social media platform.

For more Home Loan information and inquiry, please call/ Whatsapp us at +6012-6946746

At MalaysiaHousingLoan.com, we offer FREE online consultations to all our visitors. Whether you need guidance on:

🏡Refinancing

🏡Buying or selling a property

🏡Mortgage insurance & lawyer fees

🏡Stamp duty & legal documents (SPA, MOT, POT, POC)

🏡Loan quotations & more

…we’re here to help! 🏡💙

Need advice? Just call or WhatsApp us at +6012-9771019 —we’d love to assist you!

Leave A Comment