Before you can start searching and looking for a house to buy, maybe the most important thing to do is to see whether can you afford to buy one and How Much Salary To Buy A House?

Some backstories about my life

When I was young, I always knew that I want to own a house. But, because I’m not born into a wealthy family, I know it can be tough to buy one. I know I will own a house one day, just… maybe it’s going to take a longer time compare to other people.

So, the next step I did was to join a bank, to be precise in a Mortgage Loan Department. I learned ways of home loan approval criteria, making sales, and all the way until the disbursement process, everything from A to Z.

Knowledge is Power.

With the knowledge I gain in my twenties, I manage to buy a few houses before the age of 30s. Therefore, I always believe knowledge is power.

I’m telling you this is not asking you to join a bank but to acquire knowledge. Knowledge is everywhere, especially in this digital world we are living in.

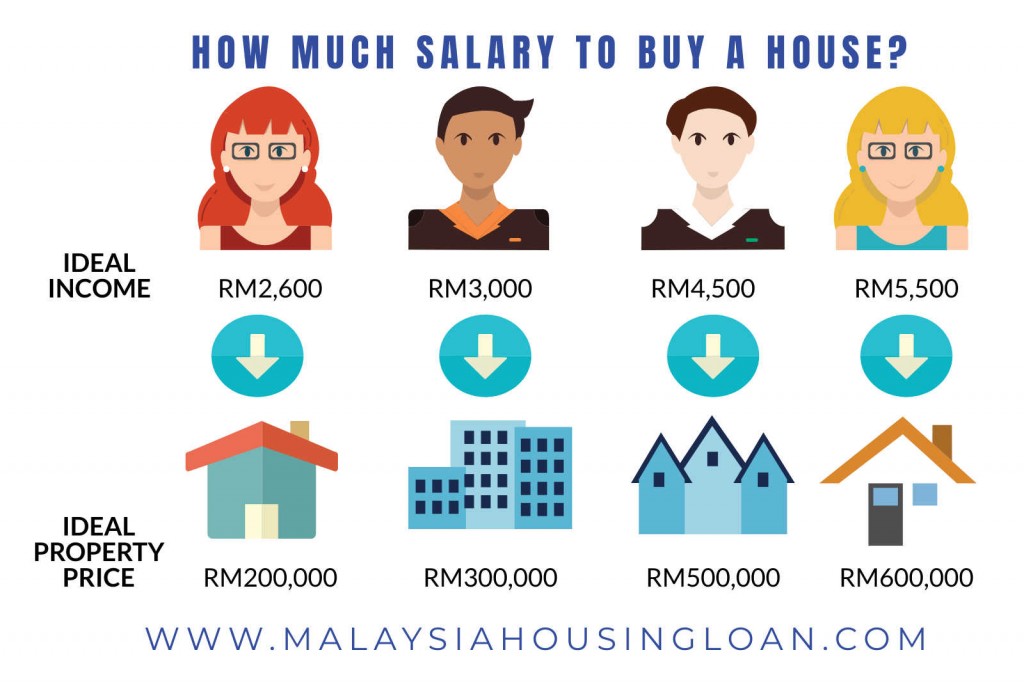

How much salary to buy a house?

Salary and commitments are essential consideration factors for your loan entitlement.

Usually, a bank will have a debt service ratio to calculate how much they should lend you. An ideal debt service ratio will be between 60%-70% of your salary.

The formula for Debt service ratio is,

(All commitments / Net income ) x 100 = should be in the range of 60%-70%

For example,

If your net income is RM3000.

The ideal Debt service ratio will be RM3000 x 70% = RM2100.

Meaning your existing commitment plus the new commitment should be within RM2100.

Let say if the house price is RM200,000. You’ll get a loan of RM180,000.

The installment for the house is RM864.00 per month.

And you have one existing commitment, a personal loan with a monthly repayment of RM1000.

So the Debt service ratio for your loan is,

All commitments : RM864 + RM1000 = RM1864.00

Net salary: RM3000

RM1864/RM3000 x 100 = 62.13% (Debt Service Ratio)

In this case, your loan most probably will approve.

Exception Guidelines

The Debt service ratio formula seems to be quite straight forward, but there is still another consideration factor when a bank is giving a person a home loan.

As we know, some banks might have a minimum entry gross salary around RM3k to RM5k to apply for a home loan. It means that even you have an ideal 60-70% Debt service ratio, but if your income doesn’t reach the minimum required income, you will not get approval.

So in order to get approval, it best for you to fulfill both requirements.

Bonus Tip:

For a person who doesn’t have any loan with a bank, you should get at least one loan with any banks. A credit card will be the best option. Use your credit card and repay it on time.

When you apply for a home loan, the new bank will base on the credit card track record to evaluate your repayment conduct. If without any loan with any bank, your loan has a high chance of rejection from the bank.

We hope you enjoy this article – How Much Salary To Buy A House?

And feel free to SHARE and LIKE, or if you have any questions about this, you can reach us at 012-6946746. We love to help!

At MalaysiaHousingLoan.com, we offer FREE online consultations to all our visitors. Whether you need guidance on:

🏡Refinancing

🏡Buying or selling a property

🏡Mortgage insurance & lawyer fees

🏡Stamp duty & legal documents (SPA, MOT, POT, POC)

🏡Loan quotations & more

…we’re here to help! 🏡💙

Need advice? Just call or WhatsApp us at +6012-9771019 —we’d love to assist you!

Leave A Comment