In this article, we cover the basic thing you should know about Standardised Base Rate (SBR) that was implemented in early august 2022 by Bank Negara Malaysia.

Standardised Base Rate (SBR) is a new framework introduced by Bank Negara Malaysia (BNM) on 1st August 2022.

The new introduction of Standardised Base Rate (SBR) is to replace the existing Base Rate (BR), where the system is more confusing to consumers.

In the past, so many people were baffled by Base Rate and Spread when comparing the bank offer.

At last, BNM uses a familiar framework as Base Lending Rate (BLR), where every bank has the same Standardised Base Rate (SBR) across the board. Thanks, BNM!

Not only that, the Standardised Base Rate (SBR) will be pegged solely to the Overnight Policy Rate (OPR). This means that if the Overnight Policy Rate (OPR) is 2.25%, so do the Standardised Base Rate (SBR). Simple!

It is worth noting that at the time of writing this article ( Date 15/8/2022), the Standardised Base Rate (SBR) & Overnight Policy Rate (OPR) is 2.25%.

Why the change to Standardised Base Rate (SBR)?

The old Base Rate framework is complicated and creates so much confusion.

Before 1st August, every bank has its Base Rate and Spread rate.

The consumer needs to figure out these two rates before deciding to take up the loan. It becomes such a big challenge for them.

To compare Base rates, the consumer must also understand how the specific bank pegs its Base Rate- another challenge!

Therefore, we welcome the new SBR framework with an open arm.

How is the new home loan interest rate calculated?

With the new SBR framework, the home loan interest rate will use the following formula as a calculation.

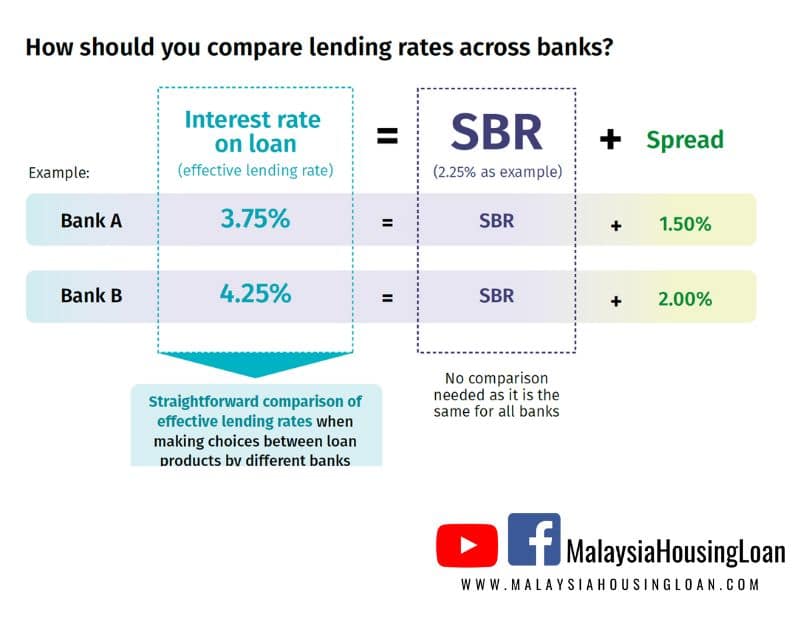

Effective Lending Rate = Reference Rate + Spread

Effective Lending Rate :

Borrowing cost of your loan or your home loan interest rate.

Reference Rate :

The Standardised Base Rate (SBR) is an example of a reference rate. It determines the changes in borrowers’ repayments on floating rate loans throughout the tenure. And Overnight policy rate (OPR) is the Standardised Base Rate (SBR).

Spread :

A spread includes credit and liquidy risk premiums, operating costs, and profit margin. A spread is usually different across banks and individuals based on each bank’s risk appetite. It is also generally fixed throughout the lifetime of the loan.

Example for Standardised Base Rate changes.

Ali has a home loan with ABC bank and was charged with the following interest rates.

3.75% (ELR) = 2.25% (SBR)+1.50%( Spread)

Effective Lending Rate (ELR) = Reference Rate (SBR) + Spread

Then after a few months, the BNM announced an increase in the Overnight Policy Rate (OPR) to 3.0%.

Now, the current interest rates will change to the new ones.

4.50% (ELR) = 3% (SBR)+1.50%( Spread)

As you can see, the SBR changed to follow OPR, the spread remained unchanged, and since SBR has increased, the ELR will increase too.

That will be how the new framework works.

Next time, when getting a new home loan, you only need to compare the spread. Easy!

Frequent Asked Question

1.If the SBR can change, affecting the interest rate on the loan, what about the spread above the SBR? Are banks allowed to change the spread during the loan tenure?

Banks are not allowed to increase the spread above the SBR during your loan tenure unless you change your credit risk profile (for example, if you fail to pay your loan repayments).

2.Why is the spread above the SBR larger than the spread above the BR? Am I being charged more given the larger spread above SBR?

You are not being charged more just because the spread is larger. This can be seen from the “effective lending rate (ELR)”, which is the interest rate charged on a loan. If the ELR is the same, you are not charged more.

However, as the SBR is linked solely to the OPR for all banks, individual banks will consider their specific business or funding costs in the spread instead, which are different across banks.

After you have entered into a loan contract, banks are not allowed to increase the spread during the tenure of the loan, except when a borrower’s credit risk profile changes. In comparison, under the BR regime, a bank may change its BR because of changes in its funding costs, which is less transparent to borrowers.

3.If I have a BR- or BLR-based loan, would it be affected by a change in the SBR?

Yes. Both BR and BLR will move exactly in tandem with the SBR. This means that for any change to the SBR, following a change in the OPR, banks will adjust the BLR and BR by the same amount of change in the SBR.

4.How long does it take for banks to adjust the SBR, BR and BLR after a change in the OPR?

Bank Negara Malaysia requires banks to adjust the SBR, BR and BLR by the same amount as the OPR within seven working days from the date of the OPR change.

5.Would my loan instalment be affected when there is a change in the SBR, BR and BLR?

Yes. When the SBR, BR and BLR are reduced, banks will reduce your loan instalment amount. Similarly, if they are increased, banks will increase your loan instalment amount.

If the change in your instalment amount is less than RM10 per month, some banks may keep your instalment amount unchanged and then adjust the loan tenure or final repayment amount accordingly. Your bank must inform you in such cases and provide details on how this might affect your loan tenure or overall interest costs where relevant.

6.When my loan instalment amount is revised, will the bank inform me?

Bank Negara Malaysia requires banks to inform borrowers of any revisions to their loan instalment amount at least seven calendar days before the new instalment amount is due for payment. Banks may communicate with borrowers via mail or electronic means (e.g. SMS, emails).

7.What happens if a borrower cannot meet the higher loan instalment amount when the SBR, BR or BLR are increased?

A borrower who is facing financial difficulty in repaying the new, higher instalment amount can request to maintain the original instalment amount.

The loan account may be classified as ‘rescheduled and restructured. The bank will inform the borrower of such classification and its implications, including:

- Increase in the total cost of borrowing;

- Extension / addition to the loan tenure;

- When to repay the additional interest amount, if any.

8.Is there any difference between whether I take a new loan before or after 1st August 2022?

- Loans taken before 1 August 2022 will still be priced against the BR (i.e. BR + spread), while loans taken from 1 August 2022 will be priced against the SBR (i.e. SBR + spread).

- Whether a loan is priced against the BR or the SBR, the interest rate on a loan (or ‘effective lending rate’) will continue to be competitively determined and influenced by multiple factors, including a customer’s risk profile and banks’ business strategy.

- Whichever the case, both BR and SBR will move exactly in tandem with the OPR from 1 August 2022 (see question 6).

9.Where can I view the SBR, BR and BLR?

- Banks will publish their SBR, BR and BLR at all their branches and websites. For new customers, banks will disclose the SBR and the interest rate on a loan (or ‘effective lending rate’) in the product disclosure sheet of the loan.

- The SBR, BR and BLR historical series will also be available on banks’ websites.

10.Where can customers make inquiries about the Reference Rate Framework or lodge complaints regarding banks’ practices?

Customers who have queries or complaints can contact their respective banks’ complaint units or BNMLINK at https://telelink.bnm.gov.my/ or 1-300-88-5465.

LIKE, SHARE & FOLLOW US!

#malaysiahousingloan

Online Mortgage Consultant

Call or Whatsapp Us: 012-6946746 (Talk to David)

Subscribe Our Youtube Channel

Follow us on Facebook

Leave A Comment