BNM Increases the OPR from a record low of 1.75% to 2.00%

How will it impact your home loan? Read this article to understand more.

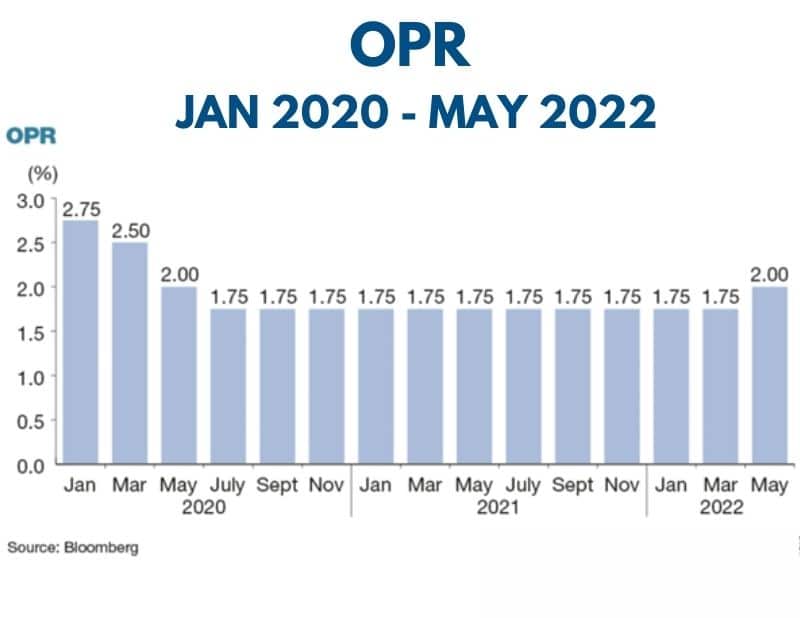

On May 11th 2022, Bank Negara Malaysia (BNM) increased the overnight policy rate by 25 basis points to 2% from a record low of 1.75% as global inflationary pressures have risen sharply.

The OPR at 1.75% is the lowest on record, according to BNM data dating back to 2004 on the central bank’s website.

What is the Overnight Policy Rate (OPR)?

The overnight policy rate (OPR) is the minimum interest rate charged amongst banks in the interbank market, which borrow funds from each other.

When a bank has a fund deficit to meet the withdrawal demand from depositors, the bank will borrow from another bank with an excess fund.

The Impact of Overnight Policy Rate (OPR)

When BNM increases or reduces the OPR rate, it will significantly impact the country’s economy.

A lower OPR effect a lower interest rates – this means the interest rates for borrowing will be lower, increasing the borrowing activities and stimulating the economy.

A higher OPR will convert to a higher interest rate that discourages borrowing activities in the market.

How does the Overnight Policy Rate (OPR) impact Home Loans?

OPR directly affects the bank’s Base Rate (BR) and Base Lending Rate (BLR).

For example,

If the current OPR is 1.75%,

Bank A adjust the BR to 2.63%

The bank might offer a customer the following interest rate.

Variable rate: BR + 0.37% p.a

Translate to 2.63+0.37% = 3% p.a

However, if the OPR is 2.00%

Bank A might adjust the BR to 2.88%

Therefore, the interest rate will adjust to 2.88% + 0.37% = 3.25%

Undoubtedly, when there is a change in OPR, the BR or BLR will change too. Hence, the adjustment of home loan interest rate.

And when there is a change in the interest rates, one of these things will happen to the home loan account.

Revision in the monthly instalment payment

The monthly instalment will most likely revise to fit the new interest rates when the interest rate increases.

On the other hand, if the interest rates reduce, the bank will also reduce the monthly instalment.

The adjustment is to make sure the borrower is entirely on track to repay their home loan within the agreeable tenure.

OR

2. Adjustment on the loan tenure

If a bank does not increase the monthly instalment, it is most likely the loan tenure will be extended to cope with the increase in the interest rate and vice versa.

What can you do now?

Firstly, check your latest home loan interest rates and the instalment amount.

You can call the bank, or if you have online banking, it will be handy.

Write down the interest rate and instalment amount.

Secondly, wait for the announcement.

After the OPR announcement, all the banks will slowly increase the Base Rate, and typically the media will widely cover it.

Or you can go to the bank website and look for any new announcement on the BR or BLR.

Once your bank has increased the Base Rate, check the new interest rate and the monthly instalment again.

Typically, the bank will also send out letters to all borrowers about the increment.

Then, compare.

Compare the previous interest rates and monthly instalments.

Note for the changes. And get ready for extra money to repay the home loan.

Sometimes if you have a shortfall in paying the monthly instalment, the bank will be considered it as not paying the monthly instalment for that month.

And this will reflect in the CCRIS report, which is not good.

So try to avoid it.

CONCLUSION

When OPR increase, there is a domino effect – BR/BLR, Home Loan interest rates and monthly instalment increases.

Always keep an eye out for the interest rate increases and instalments to avoid paying short.

When borrowing cost increases, the cost of owning a house also increases.

There is nothing we can do to avoid increased interest rates in the future or even now.

So, try focusing on what we can control. We can control our income by finding a way to increase our earnings or control our spending.

We hope this article is helpful and valuable, and if you guys have any further questions, feel free to WhatsApp or call us at +6012-6946746.

At MalaysiaHousingLoan.com, we offer FREE online consultations to all our visitors. Whether you need guidance on:

🏡Refinancing

🏡Buying or selling a property

🏡Mortgage insurance & lawyer fees

🏡Stamp duty & legal documents (SPA, MOT, POT, POC)

🏡Loan quotations & more

…we’re here to help! 🏡💙

Need advice? Just call or WhatsApp us at +6012-9771019 —we’d love to assist you!

Leave A Comment